Introduction

When you deposit money into your bank account, have you ever wondered: Is my money just sitting there waiting for me?

The short answer is no—and that’s actually by design. The system that makes this possible is called

fractional reserve banking, and it’s one of the core pillars of modern finance. In this post, we’ll break it down in everyday language so it actually makes sense.

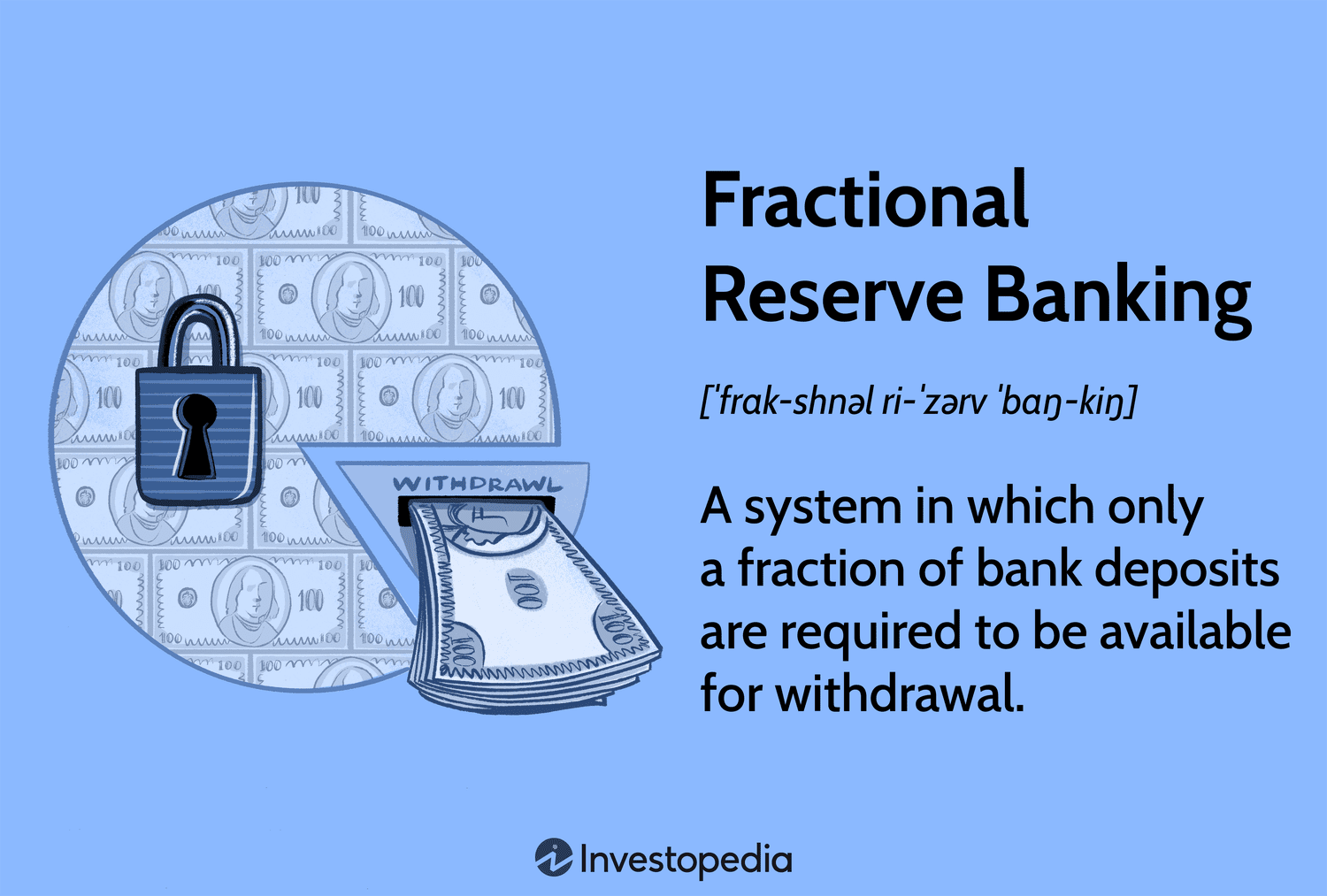

What is fractional reserve banking?

Fractional reserve banking is a system where banks keep only a fraction of customer deposits in reserve (available as cash), and lend out the rest.

You can still withdraw your money when you need it, but behind the scenes, most of it is being used to fund loans—like mortgages, car loans, and business financing.

Simple definition

- You deposit money.

- The bank keeps a small portion in reserve.

- The bank lends out the rest to other customers.

This is how banks help

create credit, support

economic growth, and earn

interest income.

A simple example: $1,000 in the bank

Let’s say you deposit $1,000 into your checking or savings account.

- Reserve requirement example:

Imagine the bank is required (or chooses) to keep

10% in reserve. - The bank keeps

$100 in reserve.

- The bank can lend out

$900 to someone else.

Now, here’s the interesting part:

- You still see

$1,000 in your account.

- The borrower now has

$900 to spend.

On paper, the system now shows

$1,900 in “money”:

- Your $1,000 deposit

- The borrower’s $900 loan

This is how fractional reserve banking helps

expand the money supply in the economy.

How banks actually hold reserves

Banks don’t keep reserves in a vault like in the movies (at least not only there). Reserves are usually held as:

- Cash in the bank’s vault, and

- Balances in the bank’s account at the central bank (like the Federal Reserve in the U.S.).

These reserves are there so the bank can:

- Handle

everyday withdrawals

- Process

payments and transfers

- Manage

unexpected spikes in customers needing cash

Why do we use fractional reserve banking?

1. It supports economic growth

When banks lend out deposits, they’re funding:

- Home purchases

- Business expansions

- Education and personal loans

This lending activity helps businesses grow, creates jobs, and keeps money moving through the economy.

2. It increases access to credit

If banks had to keep

100% of deposits in reserve (called

full-reserve banking), they couldn’t lend nearly as much. That would mean:

- Fewer loans

- Higher interest rates

- Less access to credit for everyday people and small businesses

Fractional reserve banking makes credit more widely available.

3. It makes banking more profitable

Banks earn most of their income from

interest on loans.

- Deposits: Banks often pay you a small interest rate.

- Loans: Banks charge borrowers a higher interest rate.

The difference between what they pay and what they earn is part of how banks make money.

What about risks—can the bank run out of money?

This is where the concept of a

bank run comes in.

A

bank run happens when a large number of customers try to withdraw their money at the same time because they’re worried the bank might fail. Since banks only keep a fraction of deposits in reserve, they don’t have enough cash on hand if everyone shows up at once.

How the system manages this risk

- Central banks: In many countries, the central bank (like the Federal Reserve) acts as a lender of last resort, providing emergency funds to banks if needed.

- Regulation: Governments and regulators set rules for capital, liquidity, and risk management.

- Deposit insurance: In many places, deposits are insured up to a certain amount, which helps maintain public confidence.

These tools are designed to reduce the chance of bank runs and keep the system stable.

How fractional reserve banking affects you

Even if you never think about it, fractional reserve banking touches your daily life:

- Your savings account: Your deposits are helping fund loans in your community.

- Your mortgage or car loan: Those loans are made possible because banks can lend out deposits.

- Interest rates: Central banks influence lending and borrowing costs, which affect your credit cards, loans, and savings.

Understanding this system helps you see:

- Why banks can pay you interest

- Why they charge interest on loans

- Why financial stability and regulation matter

Conclusion

Fractional reserve banking can sound intimidating, but at its core, it’s simply this:

Banks keep a small portion of deposits on hand and lend out the rest to power the economy.

It’s the reason you can get a mortgage, a business loan, or a student loan—and also why financial stability, regulation, and trust in the banking system are so important.