What Is a Fixed Index Annuity?

Setting the Stage

Before we tackle participation rates, let’s briefly clarify what FIAs are and how they fit into your retirement toolbox. A fixed index annuity is a financial product offered by insurance companies that combines principal protection with the opportunity for gains linked to a market index, like the S&P 500, Dow Jones, or Nasdaq. Unlike investing directly in the stock market, with FIAs your money is not actually invested in stocks or bonds. Instead, your returns are linked to the performance of a specified index, providing the potential for higher returns than a regular fixed annuity (which pays a guaranteed but usually modest rate) while still offering protection from market downturns. In simple terms, FIAs let you “ride along” with market growth but shield you from market losses.

Key features:

- Principal protection: Even if the market goes down, your annuity value won’t decrease due to poor market performance (though withdrawals and fees may affect value).

- Market-linked growth: Your gain is determined in part by how well your chosen index performs.

- Limiting factors: Your upside (the amount you can gain from market growth) is typically limited by participation rates, cap rates, or spreads.

It’s this last point—how upside is calculated and limited—that brings us to participation rates, the focus of our blog.

Defining the Participation Rate in FIAs

So, what exactly is the participation rate in the context of a fixed index annuity?

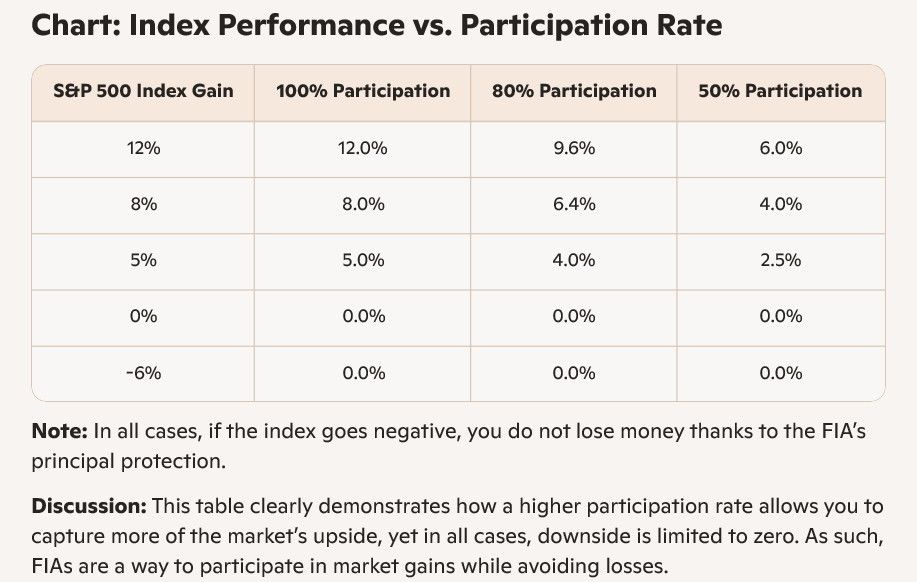

The participation rate is the percentage of an index’s gain (over a set period, typically one year) that an insurance company credits to your annuity account.

- If the participation rate is 100%, you are credited with the full percentage increase of the index (subject to any caps or spreads).

- If the participation rate is 80%, you're credited with 80% of any index increase.

- If the index goes down or doesn't increase, depending on the product, your credited interest may be zero, but you don't lose your principal.

In plain English: If the chosen market index increases by 10% in a year and your participation rate is 80%, your account is credited with an 8% gain (80% of 10%).

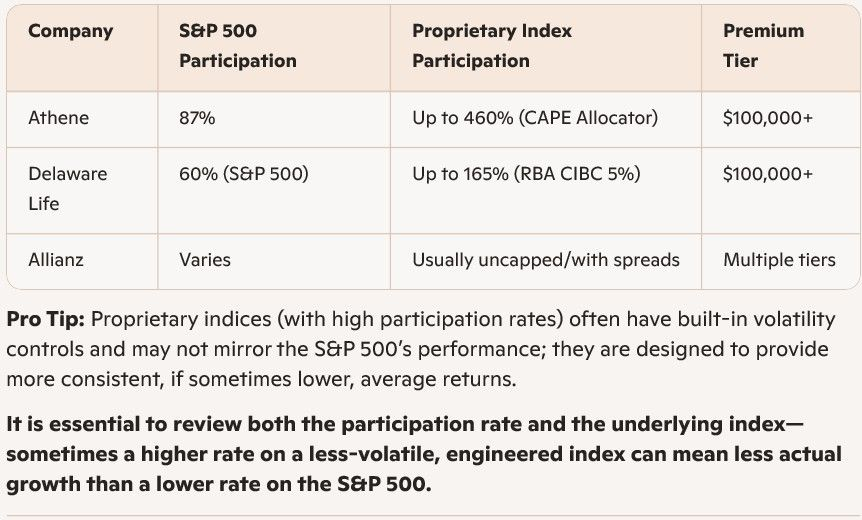

The participation rate is typically set by the insurer and is detailed in your annuity contract. In many cases, it can be reset annually or periodically at the insurer’s discretion, so it’s important to understand both the initial rate and whether (and how often) it can change.

Visual Analogy:

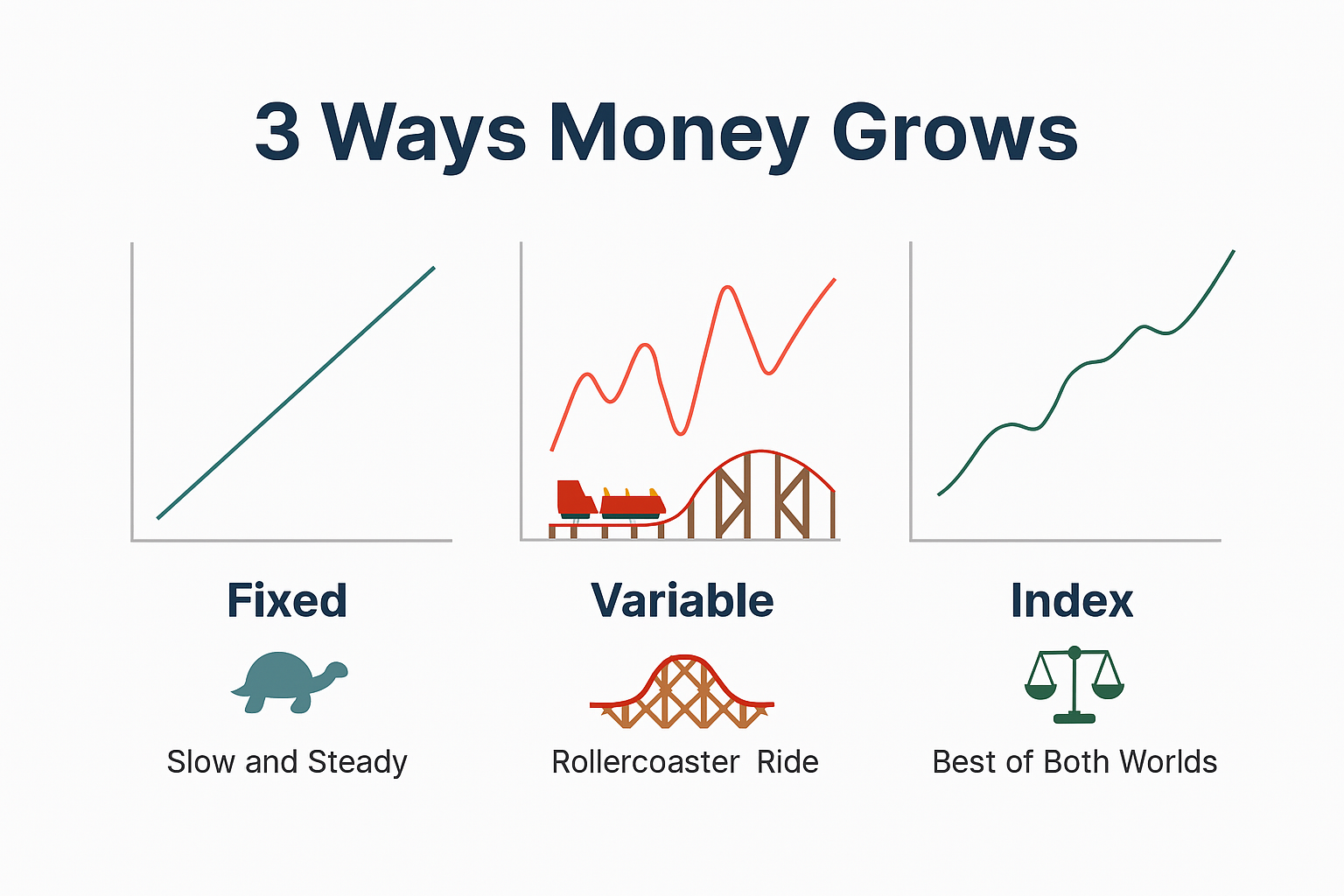

Participation Rate as a Ticket to the Market’s Roller Coaster

Imagine the index is a roller coaster at an amusement park, zooming up and down throughout the year.

A fixed index annuity is like having a ticket that lets you experience only part of those thrilling ups, but none of the scary drops.

- The

participation rate is like the height restriction on the roller coaster: it limits how much of the ride’s highs you can experience. If it’s set at 80%, you only get 80% of the way to the top on each ascent.

- Importantly, you never go down with the drops (market declines)—you simply stay where you are.

This ensures the ride is both more predictable and less risky.

Participation Rate vs. Other Limiting Features:

How It Fits In

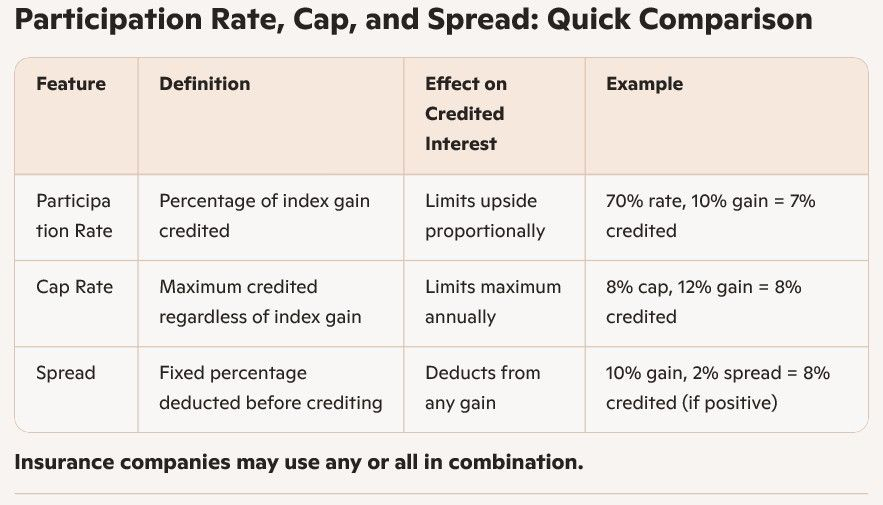

The participation rate is one of several features that insurers use to calculate how much of the market’s return you get. The main types of limiting factors in FIAs are:

- Participation Rate: As defined, the percentage of index growth credited to your account.

- Cap Rate (Interest Cap): The absolute maximum amount of interest you can earn, regardless of index performance.

- Spread (or Margin/Asset Fee): A fixed percentage that is deducted from the index’s return before your participation rate is applied.

In some contracts, you may see just one of these features; in others, you may find two or even all three limiting your credited interest. For example, a contract could have an 80% participation rate

and a 7% cap—if the index goes up by 12%, first you get 80% of that (9.6%), but the cap would reduce the credited interest to 7%.

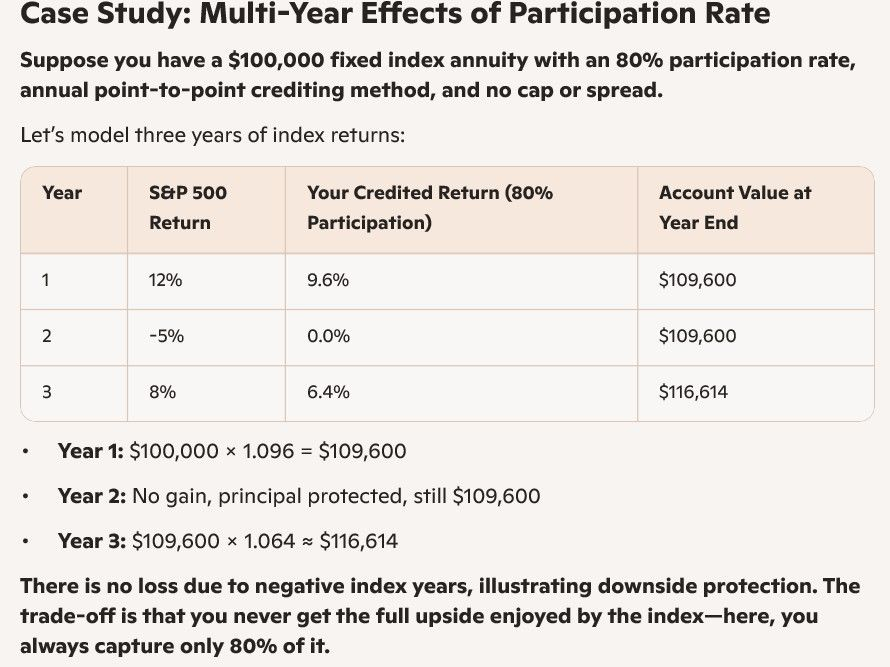

Simple, Step-by-Step Example:

How Participation Rate Affects Returns

Let’s walk through a hypothetical case:

Scenario

- You invest $100,000 in an FIA tied to the S&P 500.

- Participation Rate = 75%

- No cap, no spread for simplicity.

Suppose, over one year, the S&P 500 increases by 10%.

Calculation:

- Index gain: 10% (S&P 500 return)

- Your participation: 75% of 10% = 7.5%

- Interest credited: $100,000 × 7.5% = $7,500

If the index drops by 8%:

- Participation rate or not, negative returns do

not reduce your account value—your principal is protected, so interest credited is 0%, not negative.

If the contract included a cap:

- Suppose there’s also a 6% cap.

- Even if the 75% participation would give you 7.5%, your maximum credited interest is 6%.

If there’s a spread:

- Example: 75% participation and a 2% spread. Index rises 10%.

- First, 10% × 75% = 7.5%. Then, subtract 2% = 5.5% credited to your account.

These combinations are common, so always check the contract details.