Learn what fractional reserve banking is, how it works, and why it matters—explained in plain English with simple examples.

Key Takeaways

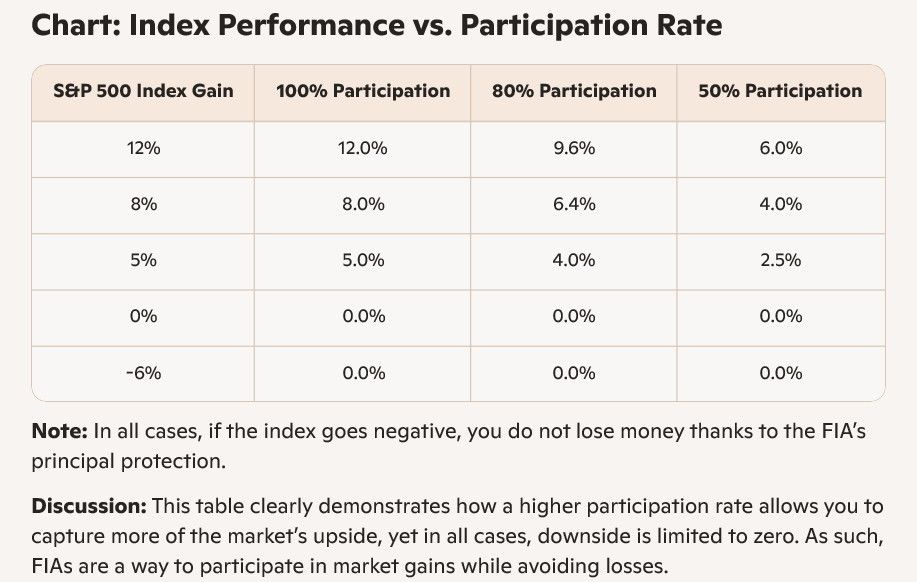

- The participation rate determines how much of the index’s positive return your FIA credits you each year.

- A higher participation rate means more upside growth, but it’s always paired with downside protection—your principal never shrinks due to market losses.

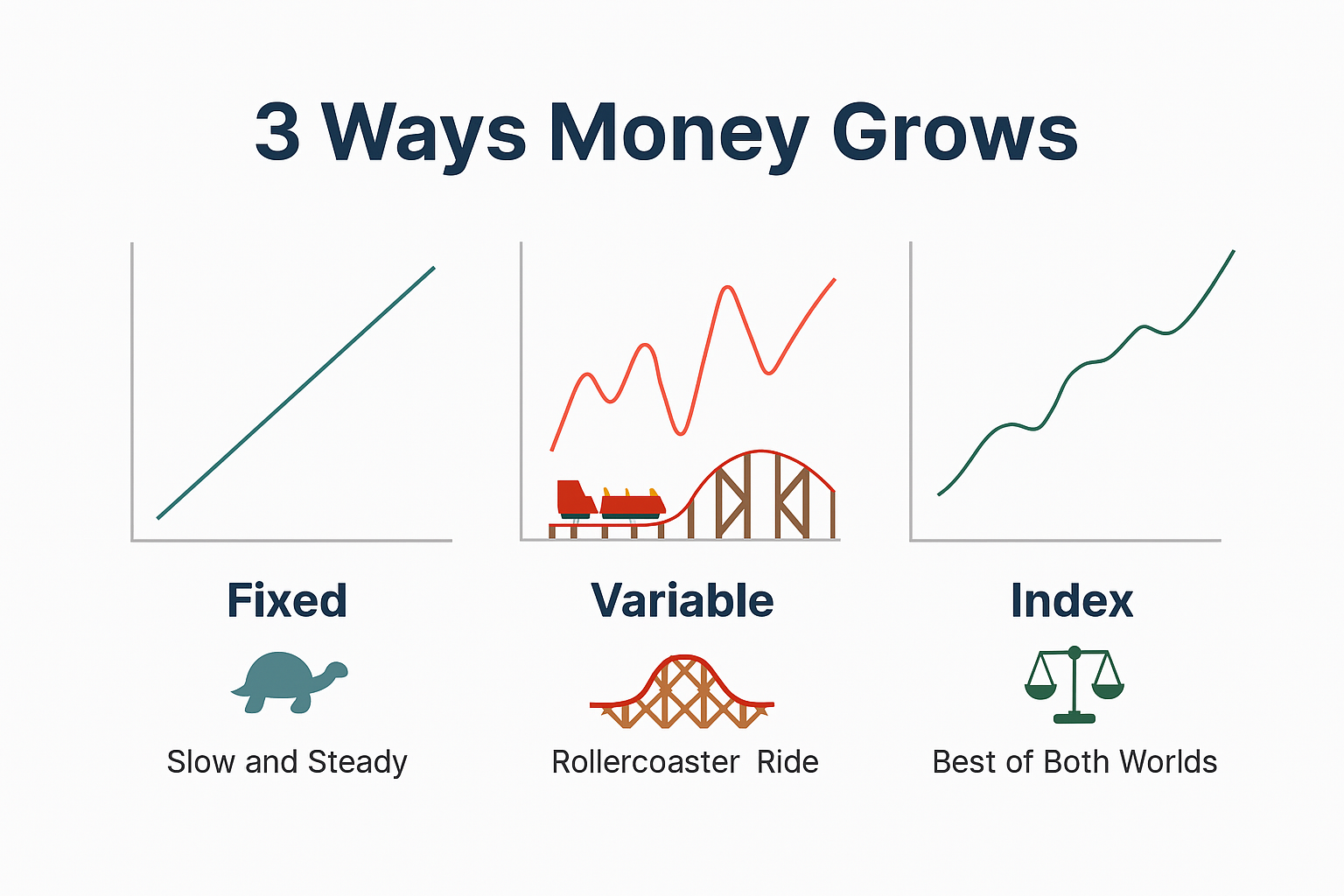

3 Ways Money Grows: Fixed, Variable, and Index

“Thinking about estate planning? Find out why a trust is smarter than a will. Explore the advantages, from avoiding probate to protecting loved ones.”

"The wealthy don’t play the same game… they play a smarter one.

💼 Own nothing. Control everything.

✅ Protect your assets from taxes, lawsuits, and creditors.

✅ Enjoy them as if they were yours.

✅ Pass them on without the headaches.

Every year you wait could mean thousands lost to taxes.

Learn how to structure your...

Led by a Certified Cryotherapies (CCT), Glacier Chill provides both onsite and mobile cryotherapy services, bringing the benefits of cutting-edge recovery right to you. Whether you’re an athlete pushing your limits, a busy professional combating stress, or someone looking for natural pain management

Business owners know one thing for certain: employees are the backbone of success. But taking care of them with the right benefits package often feels like walking a tightrope between affordability and quality. Traditional employee benefits come with hidden costs—

What’s Next?

At Master Wealth Builders LLC, we believe in helping business owners work smarter, not harder. One of the most powerful ways to do that today is by bringing artificial intelligence (AI) into your daily operations. Far from being futuristic or intimidating, AI is now accessible for businesses of every size—and when used

Discover the role of cryptocurrency in the finance sector, from blockchain basics to crypto payments and investments. Learn why digital money is shaping the future—and how to get started with a free consultation.